Game over, man. Talking about death is never something people are dying to do, but I still encourage my clients through this process because it is a major topic that needs to be covered in order to ensure your family has a well-rounded plan. Not only should they think about what great things they want to accomplish in life, but how they want others to be impacted after they are gone. It is critical to talk about these possibilities so that you can come up with a game plan of how you would want different events to play out even if you are not around to control the outcome. I want to provide a guide for you on how to navigate the estate planning conversation.

Fast Travel Links

Two of the Overlooked Reasons to Have Estate Documents:

Guardianship for child(ren) or pets:

Did you know that if you died, it is up to the state to decide who your child(ren) live with? I do not know about you, but I would try and do everything I could to make it clear who I would want my son to live with if something were to happen to both my wife and I. Without naming a guardian for your children, it is also significantly easier for others to maneuver and to try and prove to the court why they would be the best fit. That could be a nightmare for families who have already likely gone through a lot. After you establish your wishes through the documents listed below, I would recommend that you share that information with the primary people that you have identified for their respective roles.

Partners:

Estate planning covers more than just death, it also addresses incapacity issues. Did you know that if your partner were unable to act on their own, you may be unable to assist in making healthcare decisions? That was a huge concern for me prior to being married because I trusted Brittany to know me better than anyone else and have my best interest at heart. Imagine if multiple parties wanted to have a say in what should happen if you were incapacitated or in a state that requires end of life discussions…. There would likely be disagreement and regardless of the outcome, future friction over the debate.

Even married couples can run into issues on the financial end if only one spouse is listed on an account. Sometimes there is a specific reason that the accounts are separated, but there are also many times when accounts are opened this way out of convenience because one spouse handles all of the financials. If that person is unable to act, the funds can be tied up at a very inconvenient time.

The Most Common Reason People Create Estate Documents:

Assets:

Assets are the most common reason that people think about estate planning documents. Over our lifetime we accumulate a lot of things. Through estate planning, you can specifically designate certain items to individuals, which is helpful if someone holds sentimental value for certain items. Again, another touchy area where friction can easily occur if nothing is accounted for through proper estate planning and loved ones start jockeying for position over various assets.

Common Reasons Estate Documents are Avoided:

Not rich yet

Federal Estate Taxes are not a concern for most Americans due to the duel household limit being $22.36 Million. However, there are certain states, including my previous home state of Illinois that carry their own inheritance taxes. In addition to that, hopefully, you have noticed from the previously outlined items that you do not have to be a multimillionaire to cause quite a commotion with your passing.

It’s too creepy to think about dying

Yes, a grim topic to cover for sure, but it does not all have to be dark and grey. You can use this as a time to reflect on all of the great memories and experiences you have created, as well as, hone in on what truly is important in your life and provide direction on how to better align your priorities with the unknown amount of time you have left. I always ask my clients what if your doctor tells you that you are going to pass away in five to ten years from now. What thoughts are going through your head? What do you want to use your remaining time to do? Where are you going to set your priorities?

What if we change our minds

Estate planning is not a set it and forget it deal. If a major life event occurs or your respective people change, you should update your documents accordingly. Even if there is not a major trigger point that activates your thought process to review your estate plan, I recommend you set a recurring five-year check in to confirm that your wishes are current.

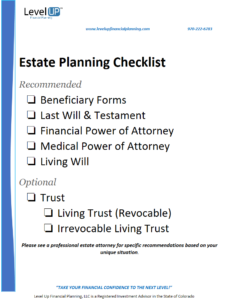

Basic Estate Documents

Beneficiary Forms

These forms are specific to your accounts at financial institutions and take precedence over anything outlined in your will. Nearly all retirement accounts require you to have at least one primary beneficiary, but almost none of your non-retirement assets require this form. That means you have to specifically have to request their beneficiary form or transfer on death forms to make sure these accounts are accounted for. Naming beneficiaries directly on your accounts increase the speed that these assets will become accessible if you were to pass away.

Last Will & Testament

Your will is the letter to the state about how you would like your assets to be divvied up and guardianship of children and/or pets after your death. Without this letter to the state, the state has their own sometimes ancient process of determining what should happen with all of your stuff.

Financial Power of Attorney

A financial power of attorney only works while you are still alive. In most cases they are utilized in case you become incapacitated or unable to act on your own for financial and legal matters. Even though you may be incapacitated, your previous obligations still need to be addressed and may require someone to step in and make sure payments are still being received and even canceling services like cable or other services that will not be needed and wasting funds.

Medical Power of Attorney

Similar to a financial power of attorney, a medical power of attorney only works while you are still alive. The medical power of attorney appoints a trusted person to make health decisions if you are incapacitated.

Living Will

A living will is also called an advanced healthcare directive. These documents layout your end of life preferences to relieve your loved ones from having to make the challenging decisions themselves.

Trust

All of the previously listed documents have a limited use that is actionable only while alive or only at death. If you have unique situations that require you to control assets well past your death, then a trust may be required. A trust allows you to set specific limitations or timelines to when assets become available to the beneficiaries named in the trust. Trusts are commonly used for families that have significant assets that they feel would be a burden or even dangerous for their beneficiaries to inherit in one lump sum. Another critical use would be for families with special needs beneficiaries who require the funds specifically cover care and may be funded with life insurance policy proceeds.

Estate Planning Conclusion

Having your wishes outlined cuts through all of the “Lucas would have wanted it this or that way” usually benefiting the person making the statement. When you write them down, your wishes are tangible and concrete and will be less likely to be misconstrued. Many people wait to address this part of their life until a similar situation hits home. I encourage you to be proactive and address this crucial part of your planning now because it creates a big stressful mess for your loved ones if you do not, should the need ever arise.

Strategy Guides Related to Estate Planning

Life Insurance for Growing Families Strategy Guide

Check out How to Choose Your Beneficiaries Strategy Guide

Want to learn more about personalized Level Up Strategy Guides?