Ready to take the leap into making a career change into coding, but unsure about how to navigate your finances? Like every other major financial decision in your life, making a career change intersects directly with your financial life. No matter where you are at in your coding career change decision, this strategy guide will help outline how to organize your finances, for your coding career change.

Take Our Free Career Change Assessment

If this is your first time reading my strategy guides, remember you can use the quick jump links below if you see your specific question.

Fast Travel Links

Getting Organized for a Career Change

Regardless of where you are at in your coding career change, you will always benefit from understanding where you stand today.

Cash Flow

Where is your money coming from and where is it going, AKA, a budget. You may be surprised that most millionaires actually review their cash flow regularly. You may have thought that they would be more nonchalant about it. On the other hand, most middle-class Americans have no clue where to start when reviewing their cash flow.

Having a general idea of where your money is going is critical in not only making wise financial decisions but also having confidence that you are making every dollar work as hard for you as you do to earn them.

The best budgets account for every dollar, but as long as you are in the ballpark, you are better off than most people.

Here is an overview of the main components of your budget:

- Income/Incoming Cash Flow:

- Savings:

- Debt Payments:

- Fixed Expenses:

- Variable Expenses:

- Non-Monthly Expenses:

Ideally, your savings should be in the double digits and you shouldn’t be going further into debt each month or needing to withdraw from your savings. This dynamic has the potential to change dramatically if you do not have incoming cash flow during a career change. Knowing where your money is going ahead of time can help you increase your savings prior to taking the leap and prune non-essential expenses during your transition.

Net Worth

You may think this is just a vanity stat, but this is arguably the most important number after how much you spend. Your income is actually the biggest vanity stat because many high-earners mismanage their finances and are in a worse position financially than lower earners who have better habits.

Initially, everyone starts essentially with a net worth of $0, or worse, a negative net worth due to the modern-day epidemic known as student loans. The name of the game is to properly turn your hard-earned money into assets over time. Like any great feat, this takes time and consistent effort. The main purpose of increasing your net worth, aside from the potential impacts of a career change, is to have assets that will work for you so that you can gain financial freedom at some point, hopefully by retirement at the latest. It is ridiculous the number of possibilities that open up if you play the game right!

Here is how to calculate your net worth:

Assets – Liabilities = Net Worth

In addition to the general purpose of building wealth, your net worth is highly important during a career change in case you need to tap assets to successfully make the transition.

Education Options for a Coding Career Change

Did you know there are more ways to become a coder than taking the traditional college route? It’s possible that alternate routes may actually allow you to achieve this goal faster and with less cost.

New Podcast: Techie Personal Finance Bootcamp!

Self Taught

You can pay for tools to help streamline your education, but there are more than enough free options to piece together your coding education. Youtube, blog posts, and Github are just a few popular tools you can leverage on your way to self-teaching yourself coding. Many also find it beneficial to create content as a form of learning and developing your coding skills.

This route may be the most challenging, but it is definitely doable. Check out this great post from Learn to Code With Me: 11 Steps to Becoming a Software Engineer without a CS Degree

Traditional College

Traditional college is still one of the most common ways to start a career. Most colleges require four years worth of courses, which usually amount to nearly $40,000 if you go to a state school. Those costs increase substantially if you need housing.

However, the landscape for education has started to shift, especially when it comes to coding careers.

Bootcamp

Coding bootcamps started sprouting up a few years ago and many of the graduates obtain positions after completing the programs. There are now various curricula available depending on your desired coding career.

The Course Report provides many great resources for you to research on becoming a coder. They recently posted an infograph that identifies the average bootcamp is 14.3 weeks long and costs $11,900.

Funding Education for a Coding Career Change

Self-Funding

There are two ways you may be able to self fund your way to becoming a coder. By selling assets that you’ve accumulated to pay for the cost of attaining the education or by earning enough income to cover your normal lifestyle costs in addition to the cost of your education. The most ideal method would be through your current income, though that may prolong the amount of time it takes for you to finish your education.

Student Loans

The most common way many attain funding for education is student loans. Depending on the program, you may qualify for government student loans. If not, then you will have to look at private student loans, which can carry a little higher interest rates and are not nearly as flexible as the government options.

Don’t forget that ultimately, you will be required to start paying your student loans off, usually within 6 months of finishing your program, but may vary. Be aware of the likely monthly payment you will owe and cross-reference that with your expected income and lifestyle expenses. If you need to adjust, it’s better to start making small improvements now.

Income-Share Arrangement

Income-share agreements are most common with coding bootcamps. They may vary, but essentially, the payment is tied to the income you are able to generate after you graduate.

This arrangement may actually cost you more in the long-term, but the benefits of an income-share arrangement are not in cost savings, but the significant risk reduction it provides. Many income-share agreements have a level of income that has to be passed before it comes into play. If your income never crosses that line, then the company you established the arrangement with will not receive anything.

Since it shifts a lot of the risk to the institution, the goal of you obtaining a great paying job and staying employed is in both of your interests. This is a glaring weakness for traditional college education where your post-graduation employment has little impact on their ability to attract future students or their ability to receive future tuition payments.

Tuition Reimbursement

Most employers provide this benefit and if you don’t see it available, ask for tuition reimbursement. This is actually something my wife and I both were able to leverage as we took a less traditional extended path to obtain our bachelor’s degrees.

The biggest snag that can occur, is if your education is unable to be tied to your current job or potentially any job that you could obtain with your current employer.

Another stipulation that sometimes is associated with these types of programs is whether or not you’d have to pay it back if you don’t serve a specific period of time after receiving the tuition reimbursement. Think about it this way though, “it’s free money towards a program you’d be attending anyway even if you had to pay back a portion or all of it.”

Parents/ Family

No Strings Attached

This is the cleanest way that a family member can help fund your education. However, I think you have to be thinking about whether your family can truly support this expense. I’ve actually seen parents and even grandparents overextend themselves financially to support a family member and it’s greatly impacted their ability to retire at their target age or with their desired lifestyle.

Alternatively, I’ve seen uncles and aunts be fortunate enough to not only cover their own children’s college expenses but those of their niece and nephews.

Family Loan

Older family members might have a lot of assets available, without the need to use them immediately. In this scenario, they may be able to temporary loan funds to you at favorable rates or virtually interest-free.

If you decide to go this route, it is best to put the details down in writing. No one wants to be in an uncomfortable agreement where the details are fuzzy and both sides are too scared to ask.

Funding Lifestyle During a Career Change

The biggest threat for you not making a successful career change is that you don’t have a long enough runway to see it all the way through. Whether it’s just a step back in income as you start from an entry-level position or if you have to dive into a 6-month bootcamp with no income. You need to make sure you set yourself up for success.

There are a variety of ways that you can build your runway. Here are a few common ways listed from best to worst. As we move down the list, you’ll see that cost and stress levels start to jump substantially:

- Savings: Saving in advance of making a major career change is by far the best way to be confident about the transition.

- Side Hustle: There are infinite ways to make some money. The problem is that most won’t pay all of the bills and most take some amount of time.

- Investments: All major investments are long-term assets. If you feel that it is highly likely that you’ll need to tap your investments in the short-term, you may want to sell assets at the current price and have the cash available. This is because the market can shift dramatically in the short-term and you may have less available in a future date.

- Home Equity: A home equity is not free, but it typically is one of the best ways to borrow at low-interest rates. (Establish your home equity line of credit before starting your career change because you need income in order to be approved.)

- Retirement Accounts: One of the last lines of defense to break in case of emergency. Retirement accounts have unique tax benefits. Unfortunately, accessing the funds early may result in fees and penalties.

- Credit Cards: Probably the most used, but the costliest and scariest route to take. If you know this is the route you are going to take, be sure to use a credit card with the lowest interest rate. You may even be able to find 0% promotion, but be aware that after the promotion the interest quickly adds up.

Adjusting to Pay Decrease During a Career Change

Reduce Excess Expenses

Remember cash flow? This is where knowing where your money is going is super helpful. If your income decreases during your career change, it will be a lot easier to identify which expenses are necessary and which are “the fat”.

Tax Planning Opportunities

Having low-income years creates a unique tax planning opportunity, that hopefully, you won’t have many in the future. As a coder, it is very possible that you will be earning a six-figure income within a few years, which means you will be in a fairly high tax bracket.

Roth Conversions

If you are in a lower income tax bracket than you had been previously and where you’ll likely be in the future, it may make sense to strategically transfer funds from a Traditional IRA into a Roth IRA.

This process increases your taxable income in the year the conversion occurs but is not penalized. Funds in the Roth IRA can then grow tax-free and can be withdrawn tax-free during retirement.

Should I Do a Roth Conversion Strategy Guide

Recognize Capital Gains

Another tax planning opportunity to consider is qualifying for the rare 0% long-term capital gains rates.

You will need to stay below $39,375 if Filing Single or $78,750 if Married Filing Jointly

Take Advantage of Pay Increase from a Coding Career Change

Making a lot more money and enjoying your coding career sounds amazing. A common thought that my clients have when they successfully make a career transition to coding is “I’m making the most money I ever have and I want to make sure I don’t waste it.”

Below is an overview that might help you prioritize your initial year or two in your new coding career.

Payoff High-Interest Debt

If you happened to pull some high-interest debt with you across the finish line to your new coding career, then it will be very important to attack these balances as a top priority.

Establish Emergency Savings

Coding and tech, in general, can be very volatile. Be sure to set up a great foundation with an emergency savings account that will give you the confidence to power through any “curve balls” life may throw at you.

Fund Retirement Accounts

Most tech companies will provide you a 401(k) retirement plan as a part of their hopefully robust benefits packages. At a minimum, you should be looking to maximize the free money, which is the employer matching percentage. It shouldn’t take long for you to drastically increase your 401(k) contribution to be greater than the minimum needed to receive your employer match. Be sure to take advantage of the great tax benefit that 401(k) contributions receive.

Consider Employee Stock Purchase Plan (ESPP)

Another great benefit that is common among publicly traded tech companies is an employee stock purchase plan (ESPP). This is a great way to obtain discounted employer stock. If you sell the shares you receive from your ESPP right after you purchase them, you are technically able to receive a guaranteed return.

Taxes do apply, but if your plan offers a large discount (some plans allow up to 15%), you will still be way ahead after taxes if sold immediately.

Want to learn more about ESPPs? Check out Understand Your ESPP Strategy Guide!

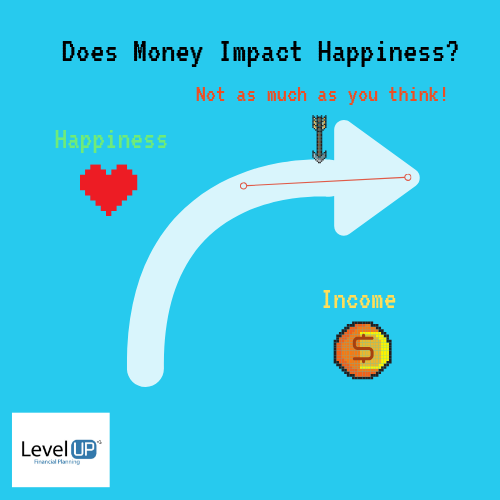

Enhance Your Life

There is a multitude of studies that show that after about $70,000 – $80,000 of income, the happiness you obtain from higher incomes greatly flat lines. The smaller incremental changes are largely due to the ability to offload unenjoyable activities or simply things we hate. Not only can you pay someone else who may enjoy these activities and rid yourself of having to go through them, but you are also creating more time for things you do enjoy.

Importance of Understanding Your Finances for Career Change to Coding

One of the common reasons that someone may fail to change career into coding is due to a lack of financial ability. As you’ve seen in this strategy guide there are ways around that, but those paths have additional challenges. Still many start down one path and run out of money to see their plan through. Establishing a solid financial game plan to support your decision to become a coder should be one of the first steps you take. This will give you the confidence to fully commit to your success down whichever path you choose to get your first job as a coder.

Connect with Level Up Financial Planning on any of our social platforms: LinkedIn Facebook Twitter

Lucas Casarez is a Certified Financial Planner™ Professional serving tech professionals virtually out of Fort Collins, CO