With the end of the tax year approaching for 2020, you may want to consider whether you should do a Roth conversion. A Roth conversion is an underutilized financial planning tool that many individuals and even financial planners overlook!

The new tax reform, which effectively lowered the tax burden for many Americans made this strategy even more attractive than in previous years. How do you know if it is the right strategy to implement this year?

We will cover everything you need to know so that you can make an informed decision on whether you should do a Roth conversion in 2019.

(Other tax planning strategy guides you may be interested in 16 Simple Year-End Tax Planning Strategies (2019), Should I Use a Donor Advised Fund Strategy Guide)

Here is a quick summary video :

Fast Travel Links

Basics of a Roth Conversion

A Roth conversion is when you strategically decide to transition funds from a traditional retirement account like a 401(k) or Traditional IRA (both before-tax income) into a Roth account (post-tax income). In this process, you need to report the conversion value as income in the year the transaction occurred.

That may sound like a raw deal, but what happens with the Roth account funds is pretty magical.

Never taxed again!

Even growth in the account is not taxed. Roth accounts are not perfect, however, you still want to analyze how the tax you pay now may compare to what you may have paid in the future.

Future Tax Expectations

Where do you expect income tax rates to be in the future when you retire? They may be higher or they may be lower.

You may feel very strongly that they may be higher. That belief could be a big driving force in your decision to start strategically paying taxes now at a lower expected rate than in the future.

If you feel they will be lower than it would be more favorable to not do a Roth conversion in 2020.

If you are like most people, you do not feel strongly one way or another and decide that you are not going to do anything.

My Two-Cents on Tax Rates

I feel rates are more likely to go up than they are to go down. Many people were shocked at the generous reduction in taxes almost across the board with the recent tax reform that was passed at the end of 2017, I was one of them!

The United States government is running at a growing deficit and there are other social systems whose budgets are not managed nearly as efficiently as they should be. This is my primary reasoning to why taxes are more likely to increase in the future.

You throw on top of the existing deficit, all of the newly printed money used for supporting our economy during COVID this year, and someone needs to pay that back eventually.

This potential of a seven-year period for lower taxes until they are set to sunset in 2025 is a great benefit for those who think taxes may be significantly higher in retirement than they may be over the next seven years.

When You Should Do a Roth Conversion

Sometimes it’s obvious that you should consider doing a Roth Conversion. Here are a few of those scenarios:

Unique Income Year

It really doesn’t matter to you where the various tax brackets land, what really matters is which tax bracket you are in. Even if you expect future tax rates may be lower when you retire, if you had a unique income year, then you may want to still consider using a Roth conversion.

A unique income year is when you receive a substantially lower income than what will be normal in the future.

There are many factors as to why this dip in income may have occurred. Some are uncontrollable negative events, but others could be great events that are worth planning for:

- Job loss: Little or no severance pay

- Sabbatical: Reduced pay or no pay

- Going from two incomes to one: (raising children, starting a business, etc.)

- A gap in employment: (pursuing education, transitioning between two jobs)

- Career transition: (moving to a new career at entry-level to work back up towards higher pay)

Related Strategy Guide: Career Change to Coding

Expect Future Income to be Greater

This is most common with younger professionals in their 20’s and 30’s, but could also include career changers too! As you progress through your career you will pick up skills and experience that can add up to significant pay raises over your working career.

As your pay increases throughout your career, you are going to be shocked by how big of a bite taxes take out of your pay. Early in your career, you are at lower tax rates, which is a great opportunity.

You may benefit substantially from making Roth contributions and Roth conversions (I will address the difference soon) during the early stages of your career.

In the short-run, you will be paying taxes now, but the long-term potential of tax-free growth could dwarf the taxes you pay now. With many areas in financial planning, you have to have a long-term view on strategies.

How to Retire Early Strategy Guide

Be Aware of Impacts

How much you are going to pay in income tax is the main factor, but you still have to consider the impact on other parts of your financial life that may be impacted by recognizing higher incomes. A few examples are the following:

- Financial aid eligibility

- Capital gains rate

- Social Security that is taxable

- Medicare surtax

- State income tax (will you potentially move from a state with a higher or lower income taxes?)

- Student loan repayments (if income-based)

- Tax credits (Limits and Phaseouts)

- Tax deductions (Limits and Phaseouts)

- Healthcare subsidies

Roth Conversions are no Longer Reversible

The tax reform at the end of 2017 ushered in a lot of individual and business tax benefits, but one of the few negative impacts was the inability to reverse your Roth conversions.

Prior to the new tax reform, you were allowed until tax filing the following year to correct a mistake. This meant that you were not required to be precise or have a detailed plan when it came to conversions. If you ran into any of the above impacts or crossed into a higher bracket than you were expecting you could simply reverse a portion of the full conversion.

This is why it makes very little sense to do a Roth conversion early in the year. Instead, wait until the end of the year to have a higher degree of accuracy.

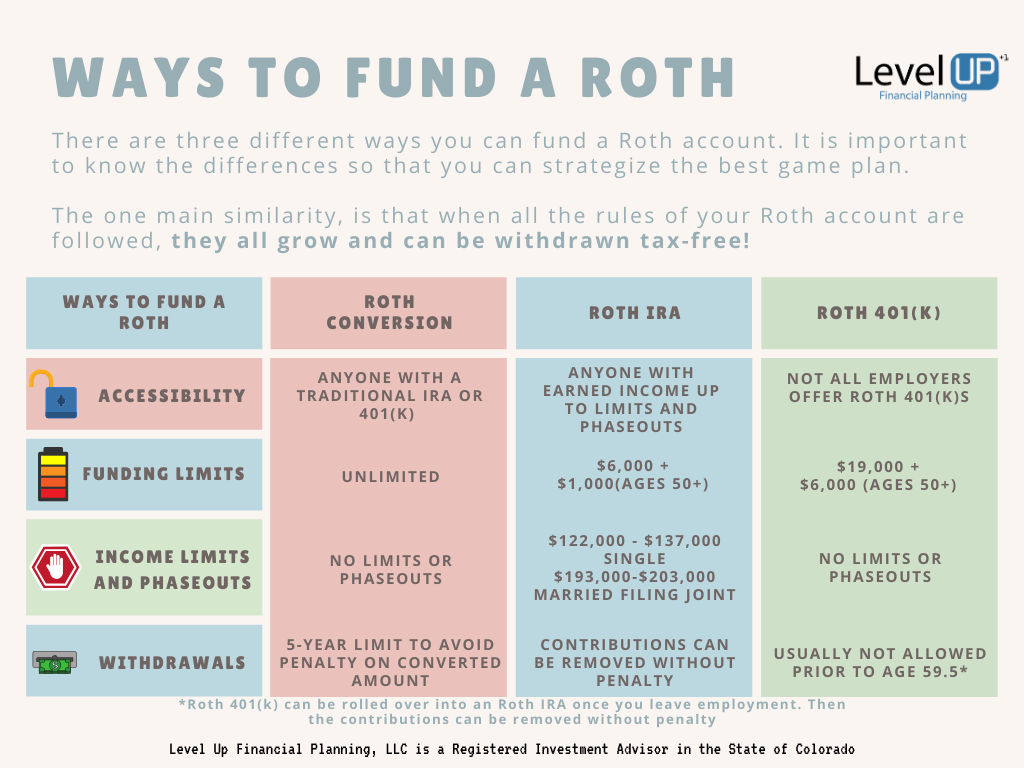

Comparing: Roth Conversions, Roth IRA, and Roth 401(k)

Roth conversions and Roth contributions are treated very differently. Here is a chart that compares Roth Conversions, Roth IRAs, and Roth 401(k)s

Does your 401(k) Allow After-Tax Contributions & Roth In-Plan Conversions?

How Much Should I Convert to Roth?

The nice thing about this strategy is that you can decide the amount you want to convert on a year-to-year basis.

One of the worst things that someone can do if they have a pretty sizable traditional 401(k) or IRA has converted it all in one year.

This would be a major fail and could shoot their tax bracket to an outrageous rate.

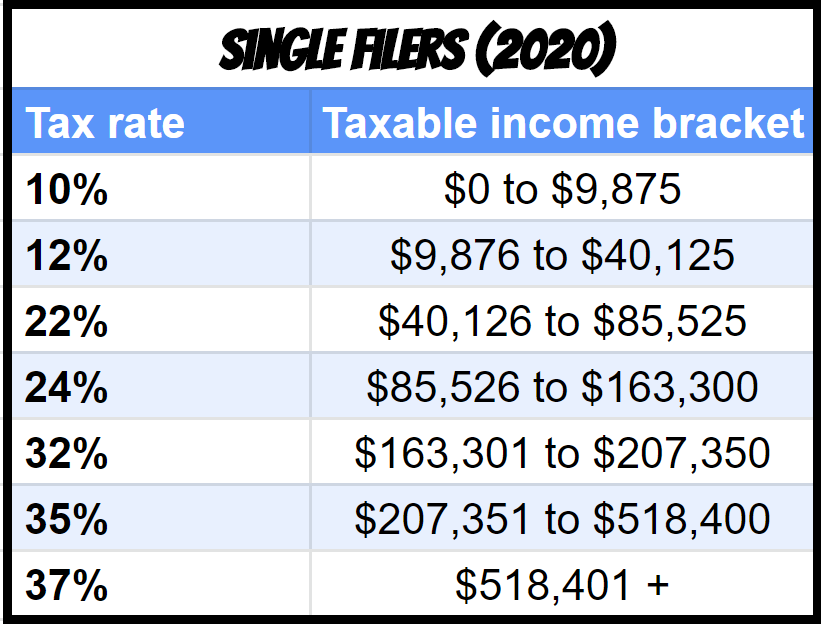

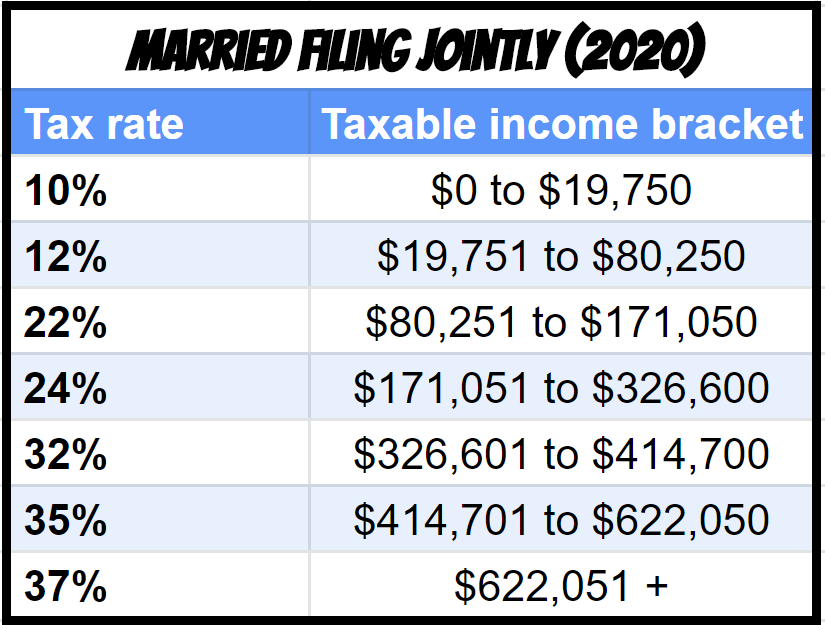

Instead, evaluate all of the factors I outlined above and decide what you will feel comfortable on. If you determine that your situation will not run into a negative scenario, then you can find your tax bracket details below for 2020.

It is a common tax strategy to fill up your tax bracket. Remember, Roth conversions are no longer reversible so you should wait to pull the trigger until the end of the year.

Find your Roth conversion tax bracket below.

How Much in Roth Should I Have?

This question should also be answered relative to the factors that we covered in this strategy guide. Having a balanced approach to the three main types of tax treatment accounts is a great strategy.

A balanced approach allows you the flexibility to navigate your future tax situation with greater control regardless of what the tax brackets look like.

The three types of tax treatment accounts are the following:

- Maybe Taxable: Non-retirement brokerage accounts

- Always Taxable: Traditional IRA, Traditional 401(k), etc.

- Never Taxable: Roth IRA, ROTH 401(k), and HSA Accounts

Why You Shouldn’t Have 100% in Roth?

I feel very strongly that you should not have 100% of your retirement assets in Roth by the time you retire.

The current U.S. Income Tax Brackets are progressive. This means the first portion of your taxable income is taxed first at 0%, then 10%, 12% and so on. If you believe the U.S. will maintain a progressive tax bracket in the future, then it not horrible to have some always taxable accounts to fill the lower brackets in retirement.

Eventually, many of my clients are taxed between 22% and 34% tax brackets. It makes sense in these higher brackets to begin to lean more toward deferring taxes with Traditional account contributions.

Here is a quick example of how you could utilize both Roth and Traditional retirement assets in retirement. If you need $120,000 in retirement and are filing jointly.

- $16,650 from Roth (0% Tax)

- $103,350 from Traditional ( Effective rate ~8.8%)

- $24,400 (@ 0%)

- $19,400 (@ 10%)

- $59,550 (@ 12%)

If you are able to defer taxes at the 34% tax bracket or even the 22% tax bracket, that is still a huge difference in tax savings.

Conclusion

Roth conversions have the potential to save thousands of dollars if used strategically. As you can see, there are a myriad of factors to weigh and consider in order to determine first if you should implement a Roth conversion and if so how much you should convert. I encourage you to work with a financial planner or tax planner to develop your tax strategy. It only takes a few strategic maneuvers to pay for the value of expert advice.

Did you hear the exciting news? Power Up Tax Planning Services has officially launched and has a few spots remaining for the upcoming tax season.

Connect with Level Up Financial Planning on any of our social platforms: LinkedIn Facebook Twitter

Lucas Casarez is a Certified Financial Planner™ Professional serving tech professionals virtually out of Fort Collins, CO