Donor advised funds have been growing in popularity recently and that was even before the new tax reform made them a critical part in your tax planning strategy. Donor advised funds are extremely versatile tools that may help you create a more tax efficient plan while still giving back to the organizations that are important to you. I will provide information on what donor advised funds are, how tax reform has increased the importance of donor advised funds, common strategies to funding a donor advised fund, and where to open donor advised funds.

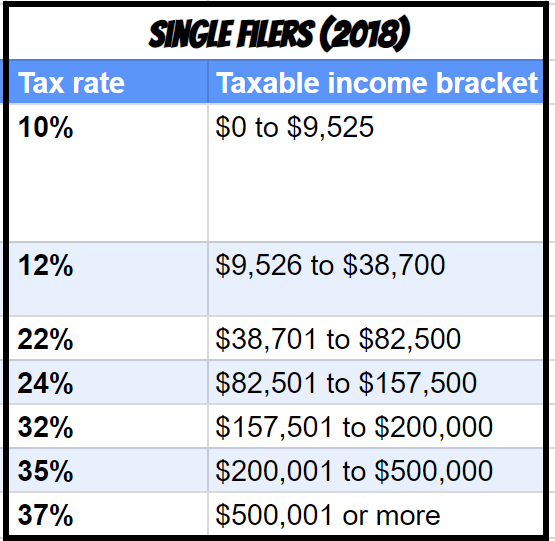

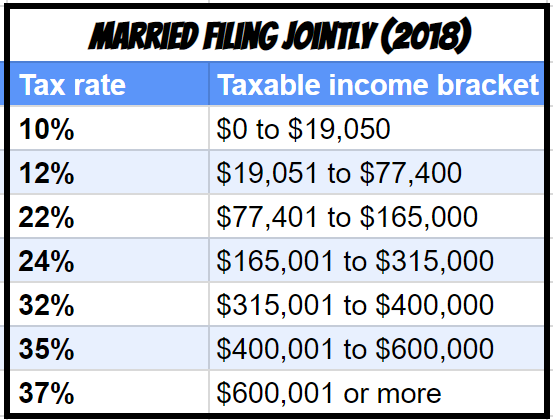

For your convenience. Here is a list of the current tax brackets for 2018.

Fast Travel Links

What is a Donor Advised Fund

A donor advised fund is an account where you can transfer assets that are to be used for charitable giving. What makes them extremely awesome and flexible is the following:

- Immediate Tax Deduction: You receive the full charitable gift deduction for the year you transfer assets into the account if you itemize.

- Control of Gifts: Although you have placed your assets into a donor advised fund, you control the distribution to charitable organizations and the years that they are made.

How is that even possible? It is because you relinquish ownership of the assets that you transfer into this account and essentially guarantee that they will be used for charitable gifting purposes even if you do not distribute funds immediately.

After you fund the account, the assets are liquidated and you may have investment options that may allow these funds to grow. Whether these assets gain or lose value, does not impact your deductibility, but obviously, it may have an impact on what you are ultimately able to gift to the organizations of your choice.

The impact from Tax Reform

The new tax reform greatly impacted the ability to itemize deductions, which is where your charitable donations would typically help on your tax returns. This may reduce or completely eliminate the tax benefits of what most individuals and families gift each year. No one ever chooses to give to charity based solely on the tax deduction potential, but I fear that many who have not followed this new development are going to be a little shocked if they end up receiving no tax benefit.

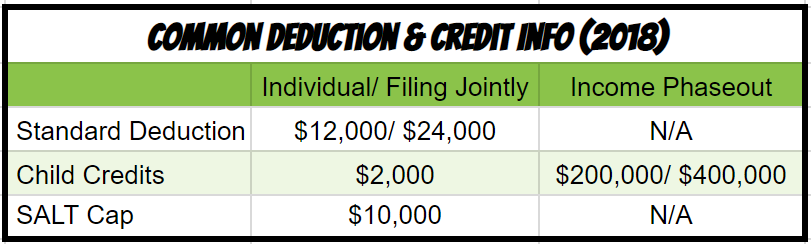

In the past, itemizing your deductions was significantly easier because the standard deduction was significantly lower and those who itemized had no problem clearing the low bar. That all changed when exemptions were scrapped from tax forms starting in 2018 and standard deductions were increased substantially to $12,000/$24,000 Single/Married Filing Joint. On top of that, one of the few blemishes on a mostly favorable tax reform is the cap on State and Local Taxes or S.A.L.T at $10,000. Weirdly enough, this cap is for both individual and married filing jointly. That essentially is a marriage penalty.

Funding Strategies for Donor Advised Funds

With a little planning, you can avoid missing out on the tax deduction benefits of charitable gifts that you plan to be making anyways both now and in the future.

Bunching

If you have the assets available, bunching is the best way to make sure you clear the standard deduction threshold. The game plan here is to fund multiple years worth of charitable giving now to receive the tax benefit for the current year. This strategy makes sure you do not lose out on the tax benefits of your charitable contributions for individual years. Remember, you have complete discretion of future distributions to charitable organizations

Appreciated Assets

You get the most bang for your buck if you contribute appreciated assets like stock and other investments that have a low-cost basis and large capital gains. This is because you gift the shares directly to the donor advised fund, which allows you to avoid paying capital gains tax. Once the appreciated assets are received, they can be liquidated tax-free and can be diversified.

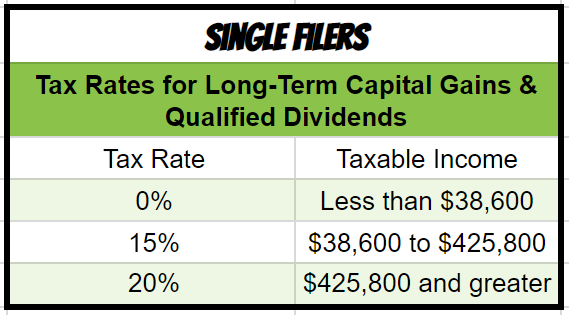

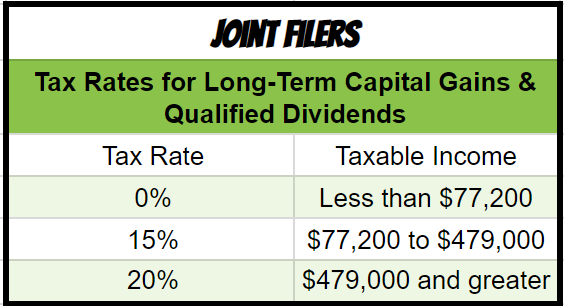

If you sell assets with long-term capital gains, the following capital gains rates apply for 2018.

Here is a quick example of why this is typically preferred over cash contributions:

Situation-

You have $5,000 market value in Intel shares that has a cost basis of $1,000. You also have $5,000 in excess cash that you could choose to gift.

If you gifted the cash to the donor advised fund and retained the Intel shares, then you receive the $5,000 potential deduction if you itemize. If you were to liquidate your Intel shares for personal use you would be subject to long-term capital gains, for this example, we can use the 15% rate. The taxes owed would be $600.

Alternatively, if you gifted the Intel shares and retained the cash, you still receive the $5,000 potential deduction if you itemize. However, if you were to use the cash, there are no tax implications and you essentially save $600 from the first example. These tax savings are magnified with larger dollar amounts and larger capital gain tax rates.

Cash

In the example above, you saw that donating cash or funds from your bank account is a pretty straightforward strategy. If you do not have highly appreciated shares, cash still works. One mistake that occurs often is that someone thinks cash is the easy way to fund their donor advised fund and liquidates appreciated stock, pay capital gains rates, and then contributes the cash generated from the sale of their stock. This is a huge mistake.

Where Should I open a Donor Advised Fund

Since they are becoming popular, I imagine that there are many options now available to open your donor advised fund. A few popular do-it-yourself companies include Fidelity and Vanguard, which have low account minimums. Working with a trusted financial planner may also make sense if managing investments is not in your wheelhouse.

The key things you should consider when choosing a custodian for your donor advised fund are the following:

Fees

Investment Choices

Ease of Use

Conclusion

A donor advised fund can add tremendous value to those who are already charitably inclined. The changes from tax reform have greatly increased the value of these unique tools and one that I encourage if you have the assets available to pre-fund future year charitable contributions today. This will help you avoid wasting possible tax deductions by missing the threshold of itemizing deductions, which many are unknowingly going to miss out on due to them not being aware of how the major tax changes impacted their charitable giving. Like any tax planning strategy, it is important to work with an expert in this area to ensure that you are optimizing your tax planning and avoiding critical mistakes.