A lot has occurred in 2020 that could impact your tax planning. Regardless of the chaos that has occurred, there are still huge tax strategies you may implement before the end of the year. Here are 15 Simple Year-End Tax Planning Strategies that can help you control your taxes.

(This list is a quick overview with basic information on each scenario. I completed additional strategy guides that dig into some of the more complex strategies I mention below. Here is a couple of them: Should I Use a Donor Advised Fund?, Should I Do a Roth Conversion This Year?)

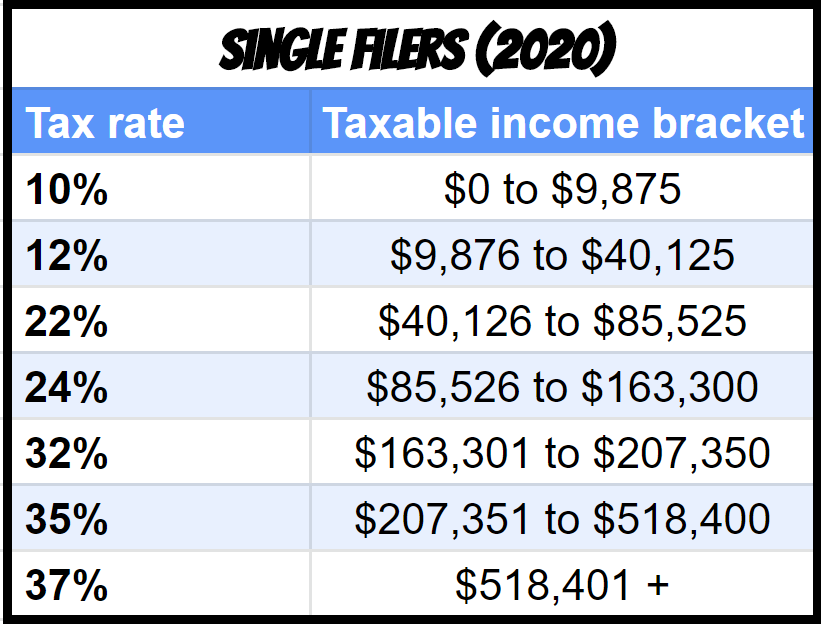

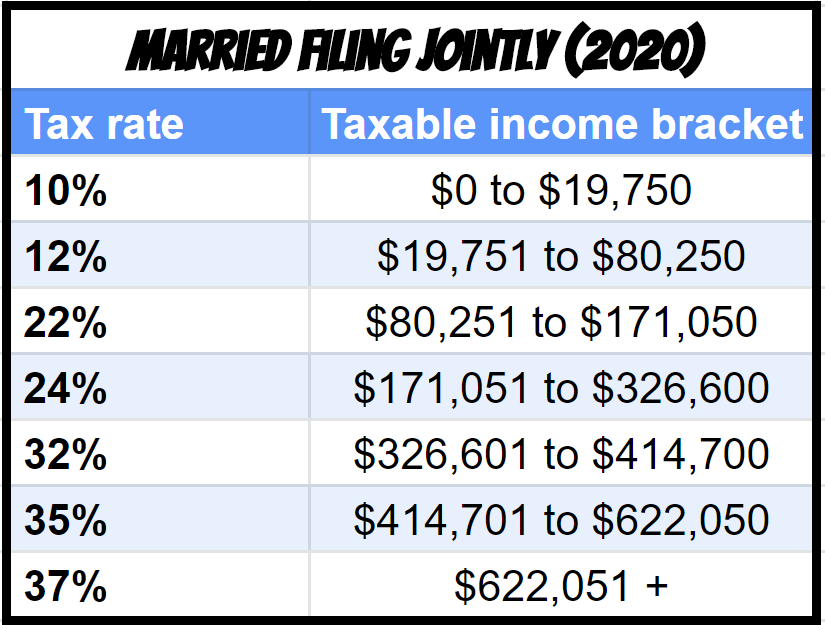

Before we dive in you may be interested in seeing the current tax brackets for 2020.

Want to see 2018’s tax brackets?

Want to see 2019’s tax brackets?

Fast Travel Links

Tax Planning Strategies: Tax Efficiency

I view tax efficiency as a way to take advantage of your unique tax situation for the current year without permanently missing out on opportunities once January 1st hits.

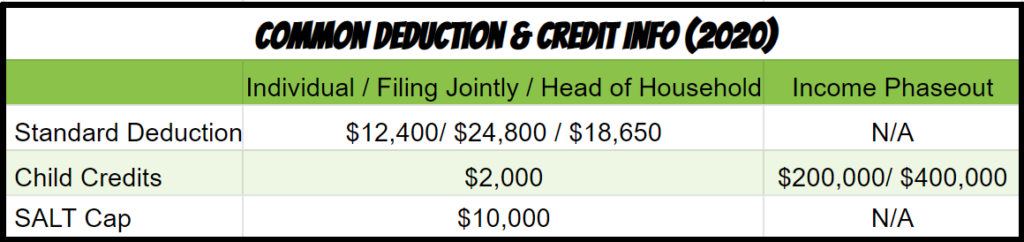

Info on a couple of Deductions and Credits for 2020.

1. Tax Loss Harvesting- Do you have investments held in a non-retirement account that have a negative value? If you sell these investments at a loss, then you can use those losses to offset gains on your other investments or some of your ordinary income.

2. Avoid Purchasing Mutual Funds- Many people do not realize how tax-inefficient many mutual funds can be. Avoid making the mistake of purchasing a mutual fund that may be forcing a significant dividend or capital gain distribution.

3. Gift-Giving- This is a popular option for those who have significant assets and are afraid that their beneficiaries may pay a large inheritance tax at some point in the future. The current gifting rate that you can do without it counting toward the estate tax calculation is $15,000 per recipient per giver. That means you can do double the amount if you have a spouse.

More on gifting tax strategies: How to Avoid the Gift Tax

4. Review FSA– Although this does not impact your tax situation, this is a strategy that avoids you wasting money. Flexible Spending Accounts are a unique benefit that you have received a tax deduction already for your contributions. Any balance greater than $500 is lost forever on January 1st, 2021 because only $500 is allowed to roll into the new year.

5. Delay IRA Distributions- This strategy is more relevant for those who are already retired. If you have already drawn a lot of income for 2020, you may want to delay large withdrawals from your account until 2021. This makes sense if you had unusually high income for 2020 and expect your 2021 income to be lower.

Tax Planning Strategies: Tax Reduction

A tax reduction strategy is something that will instantly reduce your taxable income.

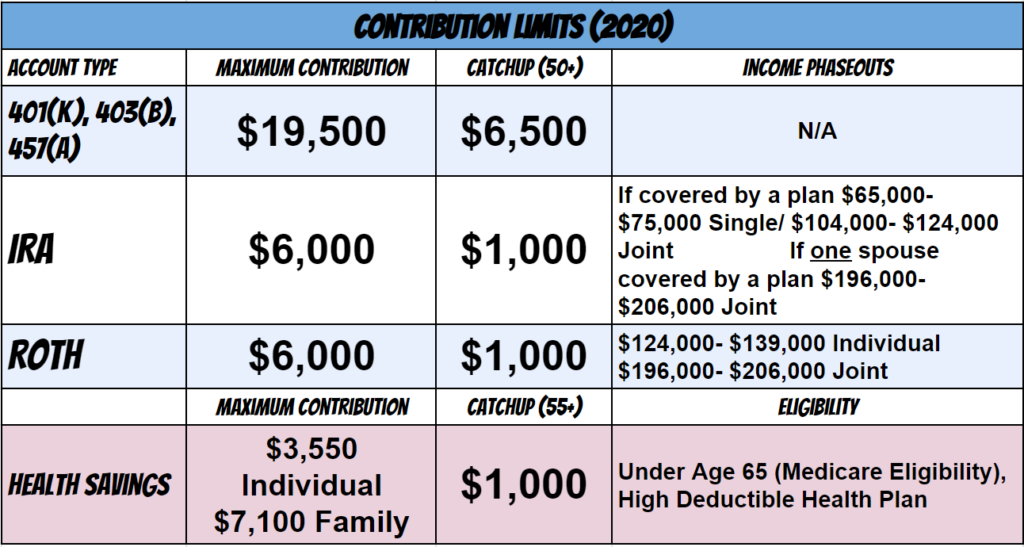

You may find this visual for contribution limits helpful.

6. 401(k) Contributions- If this strategy makes sense, you do not have much time to make the changes. Your 401(k) only allows you to contribute through your paycheck and may have a paycheck delay before it is active.

7. IRA Contributions- If you are eligible to make deductible contributions (there are income phaseouts), this strategy is a great alternative to end of year 401(k) contributions. You have the flexibility to fund this account however you want and also have until the tax filing date of April 15th, 2021. Be sure that any contributions made in 2021 that you want to be applied to 2020 are categorized accurately when you make your deposit.

8. HSA Contributions– If you are using an eligible High Deductible Health Plan, then you can contribute to a Health Savings Account and receive a tax deduction. Unlike IRA and 401(k) accounts, your funds are withdrawn tax-free if they are for qualifying health expenses. Unlike the FSA account mentioned previously, your balance in the account does not have to be spent down in order to avoid losing your funds. These are a no-brainer if you have already accumulated medical expenses for 2020. This is because you can easily contribute to your account and then turn around and reimburse yourself for those expenses.

9. Charitable Giving- It is super important to be aware that because of the new standard deduction, you may no longer receive a tax benefit from your normal charitable giving. Charitable giving may be one of the easiest ways to bunch your itemized deductions. Not only can you simply pull future year charitable giving to the current year, but you can also pool these itemized deductions into a donor-advised fund, which allows you to take the deduction for the current year but control the distributions to occur over time both now and in the future.

Tax Planning Strategies: Tax Neutral

A tax neutral strategy is one that will not necessarily reduce or tax situation for 2020 but will allow you to reposition assets into accounts that better fit your long-term financial plan.

10. Roth 401(k) Contributions- It is a shame that many employers do not offer this option, especially if you are a young professional at a lower tax bracket than where you project to be in the future. Like the Traditional 401(k) contributions, you do not have much time to make this work for you since the contributions need to come directly from your paycheck.

11. Roth IRA Contributions- You want to make sure your income does not exceed phaseout thresholds. Just like IRA contributions, you can fund this account any way you prefer and have until the tax filing date of April 15th, 2021. Confirm your contributions are categorized for the 2020 tax year.

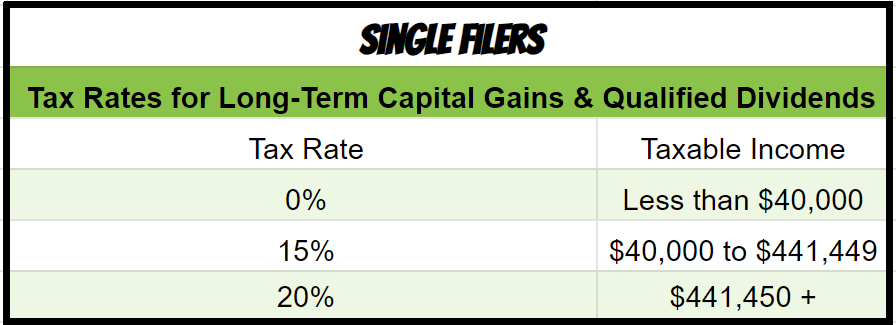

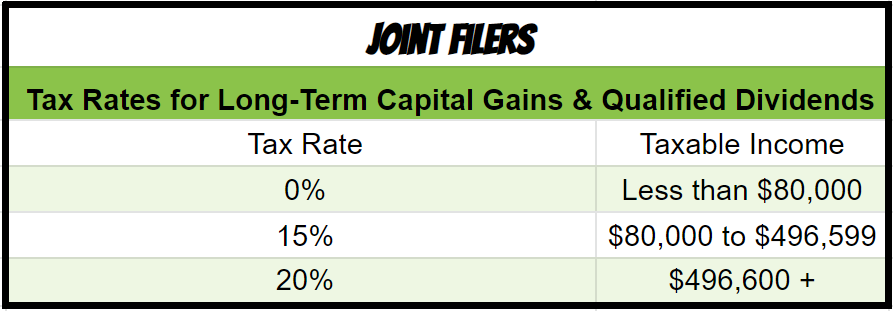

12. Selling Non-Qualified Investments/Contribute to Tax Deductible Account- One of my favorite strategies that not many planners or accountants implement with their clients is the tax rate arbitrage of selling non-qualified investments and contributing the proceeds to tax-deductible accounts. This makes sense if you are in a higher tax bracket than the long-term capital gains (see brackets below) rate that will apply to your sales. The biggest catch is that your contributions to income deductible accounts means you will not have access to those funds until retirement or until you incur medical expenses in the case of an HSA account.

13. Backdoor Roth- An advanced tax planning strategy that many implements, if they are facing the income phase-out limits for regular Roth contributions and their contributions to IRAs, are non-deductible. There is way too much to dig into here, but here is a quick overview: Contribute to IRA when your contributions would be non-deductible due to income phaseout limitations. Next, you implement a Roth conversion. I will be sure to crank out a new strategy guide that focuses on the ins and outs of this strategy.

Tax Planning Strategies: Increase Tax for Strategic Planning

Why would you want to increase your tax? Maybe if you feel that your future tax rate will be greater than it is today. Strategically maneuvering assets into a Roth or out of non-diversified employer stock may be a great strategy for your long-term financial plan.

14. Roth Conversions- (See: Should I Do a Roth Conversion This Year?) This tax strategy is great to implement if you expect your future income to be taxed at a higher rate. Another time this strategy is attractive is if you experienced a unique situation where your income dropped either from a career change or a gap in employment. One of the biggest regrets that my clients in their 30’s and 40’s share with me is that they did not make Roth Contributions earlier in their career. Unlike Roth Contributions, there is no income limit to implement Roth Conversions, though there may be an income level where you experience diminishing returns. There also is no cap on the conversion amount.

No conversion limits

Does your 401(k) offer after-tax contributions and Roth in-plan conversions?

15. Exercise Stock-Options- Depending on your current tax situation, you may wish to exercise your stock options prior to the end of the year and recognize the taxable income that is generated by the difference in the current price of your stock and what you paid for it. This makes a lot of sense if you expect your taxable income to be greater in 2020. See the tax reduction strategies above to offset and limit the tax impact of exercising your employer stock.

Tax Planning Strategies: Conclusion

Year-end tax planning in 2020 is a huge opportunity to take advantage of any of the above strategies that match your current financial situation. If one of the above strategies applies and you fail to implement you could be leaving thousands of dollars on the table that you will never get back. You may have noticed that although the strategies above are generally easy to understand if they apply to your situation, they may not be simple to implement on your own. Be sure to work closely with your financial planner or accountant to avoid making a planning mistake.

Need tax planning or tax filing assistance? We recently created an additional business to support our existing clients with their complete tax needs. Visit Power Up Tax Planning Services.

Connect with Level Up Financial Planning on any of our social platforms: LinkedIn Facebook Twitter

Lucas Casarez is a Certified Financial Planner™ Professional serving tech professionals virtually out of Fort Collins, CO

As always, I would welcome the opportunity to help you with your tax planning and more importantly a plan that allows you to take your financial confidence to the next level!